- 401 Frederica Street, B-203

- Owensboro, Kentucky 42301

- (270) 685-2652 | FAX (270) 685-6074

Strengthening Social Security:

Ideology or Economics? Modest Adjustments or Massive Overhaul? Will the debate dwell on higher returns and private control of retirement funds or effective and fiscally responsible steps to balance the books?

| History/Background | |

|---|---|

|

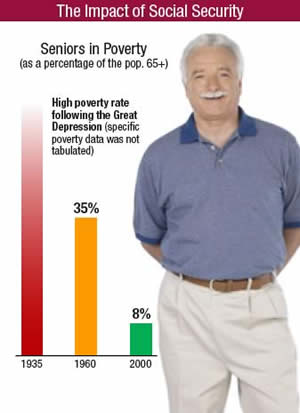

In 1930, millions of senior Americans (65 years or older) had been thrust into poverty following the stock market crash a year earlier. Only 15 percent of American workers were covered by retirement plans. President Franklin D. Roosevelt responded to these conditions by calling for our first national retirement system. Rather than draw from the federal government’s general fund, FDR insisted on a self-financed system. Social Security payroll deductions started in 1937 and the first benefits were paid in 1942. Opposition from the likes of conservative politician Barry Goldwater, economist Milton Friedman, business giant Henry Ford, and Hearst newspapers did not stem the popularity of the program. By 1960, the senior poverty rate had dropped to 35 percent. Today, less than eight percent of our seniors live in poverty. Without Social Security, officials estimate the senior poverty rate would be 48 percent. (Some groups challenge that conclusion and claim that if Social Security did not exist, people would have more of their own money to invest and save.) In the beginning of the program 10 workers paid taxes to support each retiree. In 1950 there were 16 workers for each Social Security recipient. Now, with 78 million baby boomers nearing retirement, three workers support each retiree. In 2031, one worker will support one retiree. In 1935, those 65 years or older comprised 5.4 percent of the population. In 2000, it was 12.4 percent. In 2034, there will be 74 million retirees, twice today’s 36 million. Life expectancy was 61 years of age in 1935. Today, a 65 year-old person can expect to live to 82. People are living longer, collecting benefits longer, and having fewer children. The initial Social Security payroll tax was two percent of wages. It is now 12.4 percent (divided between employer and employee) up to $90,000 of income. Through the years, lawmakers increased benefits; added an early retirement option at 62; added self-employed and agricultural workers, widows, survivors, and disabled individuals as beneficiaries; and increased the eligibility age in phases from 65 to 67.

|

Today, 53 percent of workers have no pension plan; 32 percent have no savings for retirement. Social Security does not provide, and was not meant to provide, a satisfactory retirement on its own, although 9.4 million Americans (20 percent of Social Security recipients) rely on it exclusively for their retirement income. Social Security payments make up more than half the income of two-thirds of American seniors. Social Security payroll taxes account for more than 25 percent of all federal revenue and payments represent more than 25 percent of all federal spending. Social Security currently pays half a trillion dollars per year in benefits to 47 million beneficiaries. The average benefit for 65 year-old is $1,184 per month or $14,000 per year. The latest census reports 12,643 Daviess County seniors 65 and older (13.8 percent of the population). More than 2,500 of them rely on Social Security as their only source of income.

|

| Current Challenges | |

|

The current Social Security Trust Fund surplus is $1.5 trillion. These funds are invested by law in U.S. Treasury securities, considered the safest investment in the world. By 2018, with the increasing number of baby boomers drawing Social Security, there will be a deficit – that is, the federal government we will be paying out more than it is taking in through Social Security payroll taxes. If no adjustments are made, in 13 years, it would have to draw on the Trust Fund. Since 1970, there have been 11 years when Social Security operated at a deficit. In those circumstances, bonds were redeemed from the Social Security Trust Fund to cover the difference without complications. |

The Social Security Administration has 40 actuaries on staff. Their best guess: if no adjustments are made, the Trust Fund would be depleted in 2042, although 70 percent of scheduled benefits could still be paid at that point without any increase in Social Security payroll taxes. The Social Security Trustees estimate that the unfinanced liability is $3.7 trillion over 75 years. Those with more optimistic views project that there will be no need for benefit cuts or payroll tax increases for 75 years. Others, such as the Cato Institute, project a $26 million unfinanced liability over 75 years. As challenging as Social Security may be, its future looks sound compared to Medicare. |